A TPD payout is money from an insurance policy that is part of most people's superannuation policy, known as Total and Permanent Disability cover.

It won’t usually affect your Centrelink payments, including a Disability Support Pension (DSP), while the money is still in your super and you are under Age Pension age (67).

What matters most is what you do with the money once you’ve taken it out.

Understanding TPD (Superannuation Insurance)

Most people never hear the term “TPD” until something serious happens to them. This section explains what it is in plain English before we look at the Centrelink aspect.

What is TPD cover?

TPD stands for Total and Permanent Disability. It is a type of insurance that pays you a lump sum if you suffer a serious injury or illness that prevents you from working. It’s often called "superannuation insurance" because of where it sits.

Most Australians have this cover built into their super fund automatically. Your fund takes a small premium from your account to pay for it, usually without you even opting in or noticing it.

You can read more about this in our guide to Total and Permanent Disability cover.

Do I have it, and can I claim it?

Many people who could claim a TPD payout never do because they don’t know they’re covered. You may be able to make a TPD claim if an injury or illness, whether physical or psychological, leaves you unlikely to return to the kind of work you are trained for.

The injury doesn’t have to have happened at work for you to claim. TPD cover usually applies no matter where or how you became unwell or injured. If you have had more than one super fund over the course of your working life, you may actually have cover from several of them.

How is a TPD payout different from Centrelink?

TPD payouts come from an insurance policy, while the Disability Support Pension (DSP) is a Centrelink payment funded by the government for people with a permanent disability. They are separate systems, and getting one does not automatically prevent you from getting the other.

There’s more information on how the two interact in the rest of this article.

How Centrelink Assesses Your TPD Payout

Centrelink works out your DSP with two tests: an income test and an assets test.

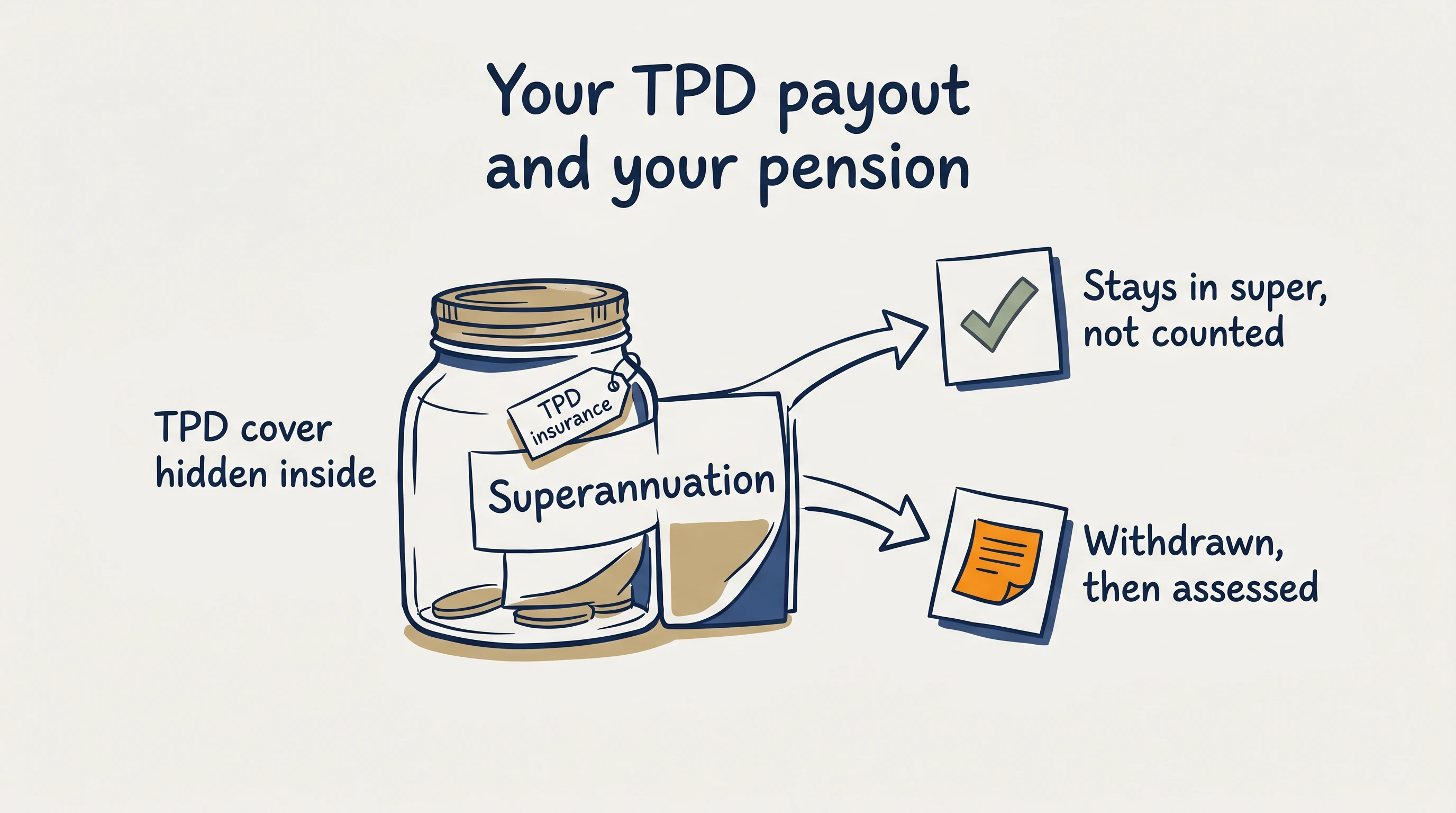

A TPD payout can affect both tests, but only once the money has left your super. The location of the money is what changes the outcome.

While the money stays in your super

While you are still too young to recieve your pension, Centrelink doesn’t count your super in the income or assets tests, as long as the fund is not paying you a super pension.

This is clearly stated on the Services Australia superannuation page, which says super is not counted "if your fund isn't paying you a superannuation pension" while you are under Age Pension age.

So, if your TPD benefit is paid into your super account and remains there, it generally isn’t considered by either Centrelink test.

Pension age in Australia is 67 for anyone born on or after 1 January 1957. Once you turn 67, the rules change and Centrelink begins counting your super in both tests.

When you withdraw the money

Services Australia is clear on this point: "Taking money out of superannuation doesn't affect payments from us. But what you do with the money may."

Once the money is taken out of a super, Centrelink looks at where it ends up:

- Money left in a bank account counts as an asset in the assets test

- Money in a bank account is also treated as earning income under deeming rules, even if the account pays little or no interest

Deeming is a Centrelink rule that assumes your savings and investments earn a set rate of income, regardless of what they actually earn. That assumed income is included in the income test.

Is a TPD Payout Treated as “Compensation”?

This is the part people most often get wrong, so it’s worth looking at in detail.

TPD payouts are generally not treated as "compensation" in the way personal injury settlements are.

Under the Social Security Act 1991 (Cth), a compensation payment is money paid wholly or partly for lost earnings or lost capacity to earn, usually from a claim for damages in cases where someone else was the cause of your injury.

These kinds of payments can trigger a compensation preclusion period, which is a set time during which Centrelink payments are reduced or stopped.

TPD benefits work differently. They are paid under an insurance policy that you funded through premiums taken from your super. Because you contributed to the policy, and because it is an insurance benefit rather than damages for lost earning capacity, a one-off TPD lump sum payout won’t usually result in a preclusion period.

The Department of Social Services has a guide on how income from personal injury insurance schemes is assessed.

If you also have a separate personal injury or negligence claim, the rules for that money are different. Our guide on how injury compensation affects Centrelink covers that situation.

Common Scenarios and Questions

Will my TPD payout stop my DSP?

Not by itself, especially while the money is still in your super. While you are under Age Pension age and the payout is in your super, Centrelink does not count it. However, if you withdraw a large sum and put it in the bank, that money is then assessed and could reduce or even stop your DSP if it pushes you over income or assets limits. Current limits can be found on the Services Australia website.

Do I have to tell Centrelink about my TPD payout?

Yes, and you should do so within 14 days. Centrelink requires you to report changes to your income and assets, including receiving a lump sum payout, within 14 days. Reporting it won’t mean you lose anything, but it protects you from an overpayment debt later, which can happen even if the payout turns out to have no effect on your entitlements.

What happens if I move my TPD payout into my bank account?

Once the money is in your bank account, Centrelink counts it as an asset and applies deeming to it. The balance of your account is assessed under the assets test, and deeming treats it as earning income. This is the main way TPD payouts can start to affect your DSP, so it is worth getting advice before you withdraw a large amount.

Does it matter what I spend the money on?

Yes. Money you spend generally stops counting once it is gone. For example, using the payout to pay down your mortgage, cover medical costs, modify your home for a disability or pay off debts reduces your assessable assets. Money you keep in the bank or use to buy an investment is still counted in the assessment. Timing and order matter, so plan before you spend.

Is my TPD payout treated like a compensation payout?

Generally, no. A one-off TPD payout through your super is usually not counted as "compensation" under the Social Security Act 1991 (Cth), so it doesn’t create a preclusion period. Compensation, according to Centrelink terms, is money paid for lost earnings or earning capacity, often from a negligence claim. TPD is an insurance benefit you funded by paying premiums, which is why it is treated differently.

What if my policy pays me regular payments instead of a lump sum?

Regular, ongoing disability payments are treated differently from a lump sum. According to the Department of Social Services, ongoing TPD or TPI payments paid from a super fund are assessed as ordinary income. This can also be important if you claim TPD and income protection together. The treatment changes with the type of payment, so this is an area where it’s worth getting early advice from an expert.

Mistakes That Cost People Their Payments

A TPD payout is often the largest sum of money someone has ever received. A few common mistakes can lead to a Centrelink debt or losing payments:

- Withdrawing the whole payout to the bank without a plan. The money then counts as an asset and is deemed as earning income.

- Not reporting within 14 days. Late reporting can create an overpayment debt even when the payout wouldn’t have affected your rate.

- Assuming super and Centrelink follow the same rules. They don’t. Your fund and Centrelink assess your situation separately.

- Spending in the wrong order. How and when you use the money affects the outcome, so the spending sequence matters.

When to Get Advice

It’s always a good idea to seek legal advice at the earliest opportunity, especially if:

- You are about to withdraw a large TPD payout and are unsure how to hold it

- You receive the DSP or another Centrelink payment and want to protect it

- You are close to Age Pension age (67), which is when the super rules change

- You have both a TPD claim and a separate compensation or income protection claim

- Your fund has offered to pay you with an income stream rather than a lump sum

There are two kinds of advice that help here. A Services Australia Financial Information Service (FIS) officer can explain how a payout affects your Centrelink payments for free.

A lawyer can help with the TPD claim itself, including whether you have cover, if the claim has been assessed correctly and how payouts affect your other claims.

You can also find out more about how a payout may affect your superannuation balance in this article.

Key Takeaways

- TPD is superannuation insurance that most Australians have by default. It can often be claimed after a serious injury or illness, though many people don’t know the cover exists.

- While the payout stays in super and you are under Age Pension age (67), Centrelink does not count it in the income or assets tests.

- Once you withdraw the money, what you do with it decides the effect. Money kept in the bank is assessed as an asset and deemed to earn income.

- A one-off TPD payout is generally not "compensation" and usually does not create a preclusion period, unlike a negligence settlement.

- Report your claim and payout to Centrelink within 14 days to avoid a later debt.

- Get advice before you withdraw or spend the money, because timing and structure change the outcome.

Get Help Now

If you think you may have TPD cover through your super, or you have a payout on the way and want to protect your Centrelink payments, Smith's Lawyers can help you understand your options. We act for people across Australia on superannuation insurance (TPD) claims.

To get started, call 1800 960 482 or enquire online. When you make contact, we listen to your situation and explain where you stand, at no cost and with no obligation, all under our No Win, No Fee, No Catch® promise.

You can also use the form below to request a free case review.