In recent years, it’s come to light that many Australians hold multiple Total and Permanent Disability (TPD) insurance policies through their superannuation funds who didn’t even realise it. If you've changed jobs over the years, you may have built up several super accounts.

Each of these could potentially contain valuable TPD insurance coverage. For lots of people, it’s now dawned on them that in the unfortunate event of becoming totally and permanently disabled, they may be entitled to claim on each of these policies at the same time.

With rising medical costs and ongoing financial pressures in 2025, understanding how to maximise these entitlements is kind of a big deal. This guide will walk you through the process of identifying, understanding, and successfully claiming on multiple TPD policies. Let’s get started with the basics.

Understanding TPD Insurance Basics

In a nutshell, TPD insurance provides a lump sum payment if you become totally and permanently disabled and are unable to work again due to injury or illness. This insurance is often automatically included in superannuation accounts, with premiums deducted from the total balance of this superannuation account (sometimes referred to as your super balance).

Learn more about what is TPD insurance claims.

The value of TPD payouts varies significantly, with the average payment amount being roughly $500,000, though it can range between $50,000 and $2,000,000 depending on the policy and your individual circumstances. Those with multiple policies can potentially receive much more than the figure just mentioned.

Each super fund (short for superannuation fund) has its own TPD insurance with different rules about what counts as ‘total and permanent disability’. And, because they’re separate, you might be able to claim from more than just one.

Always keep this in mind as you could stand to receive a whole lot more than you first thought.

Why Multiple Claims Are Possible

So let’s break this down further. As mentioned above, one of the most common misconceptions about TPD insurance is that you can only claim once. In reality, if you have multiple super funds with active TPD policies, you can potentially claim on each one for the same condition.

But, how is this possible? The reasons are simple:

- Each TPD policy is a separate legal contract

- Making a successful claim on one policy doesn't affect your eligibility for others

- And, there's no legal concept of ‘double dipping’ when it comes to insurance policies you've actually paid into

Legal experts explain it like this: ‘Making a successful TPD insurance claim against one policy has no effect on any other TPD insurance you may have, but you'll need to submit a separate claim against each policy’.

That said, in rare circumstances, some policies might contain specific exclusions that could affect multiple claims. This is why reviewing all your policies carefully is a must. If there’s just one document this year where you read the small print, let it be this one.

Identifying All Your Potential TPD Policies

Before you can maximise your entitlements, you need to identify all your potential TPD policies. Let’s take a look at how to go about this:

- Check all your super accounts: According to the ATO, approximately 4 million Australians have more than one super account, increasing the likelihood of having multiple TPD policies.

- Contact previous employers: Request information about which super funds they contributed to on your behalf. Most will be happy to assist you.

- Use the ATO's services: Log into myGov and access ATO online services to view all your super accounts in one place.

- Search for lost super accounts: The ATO can also help you to locate ‘lost’ super accounts you may have forgotten about. It’s well worth enquiring with them on this.

- Verify active coverage: Contact each fund you’re part of to confirm if TPD insurance was active from the point when you were registered as being disabled. Recent changes to the law mean insurance on inactive accounts (where there has been no contributions for 16 months or more) may have been cancelled unless you opted to stay in.

- Request policy documents: Ask each fund for the complete policy wording, definitions, and exclusions so you can assess the eligibility yourself and potential benefit amounts. Having these documents and getting to grips with them can be a real time-saver.

Understanding Different TPD Definitions

So, how do we go about making a successful claim on multiple policies? One important thing is understanding the different definitions of TPD that may apply. These definitions can vary significantly between insurers and policies, but, the most common include:

- Any occupation: You must be unable to work in any job suited to your education, training, or experience.

- Own occupation: You must be unable to return to your specific occupation.

- Activities of daily living: This criteria is based on your inability/ability to perform basic daily tasks.

Some policies may also include clauses for partial disability or have specific waiting periods before you can claim.

To identify which definition applies to each of your policies:

- Review the policy wording carefully

- Look for sections titled ‘Definition of Total and Permanent Disability’

- Note any variations in language between policies

- Pay attention to exclusions and qualifying periods

Through an understanding of these differences you’ll be able to tailor your medical evidence and approach to satisfy the specific definitions set out for each policy.

The Multiple Claims Process

Managing multiple TPD claims requires careful organisation and strategic planning, but we’ve got you covered with this helpful step-by-step approach:

- Identify all eligible policies: Confirm which policies were active when you were first registered as disabled.

- Review each policy's requirements: Different insurers have different forms, documentation requirements, and processes. Go through each carefully and write down exactly what each requires.

- Prepare separate claim forms: Complete individual applications for each fund, ensuring you meet all their specific requirements.

- Gather comprehensive evidence: Collect medical reports, employment records, and other supporting documentation to match each policy's definition of TPD.

- Consider the order of claims: In some cases, the order in which you lodge claims matters. Some legal experts recommend strategic timing to avoid having evidence from one claim potentially undermining another.

- Keep detailed records: Maintain separate files for each claim, including all correspondence and documentation.

- Be prepared for delays: Each claim can take several months to process, with variations between funds. Make sure to follow up at regular intervals to keep track of the progress.

A common challenge mentioned by applicants who we’ve spoken to is handling overlapping requests for information while making sure what you hand over specifically addresses that policy's definition of TPD. It can be a minefield, but using the simple steps above will put you on the right track.

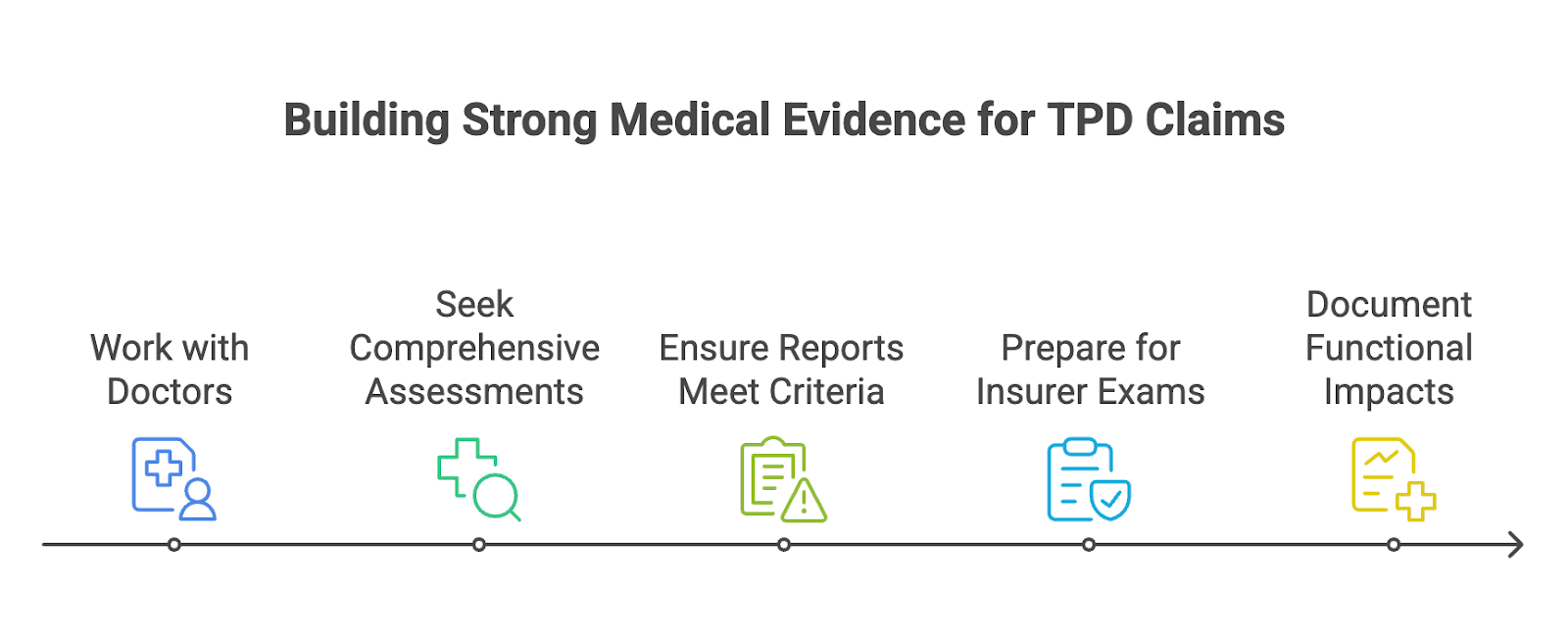

Building Strong Medical Evidence

The success of your TPD claims largely depends on the quality and relevance of your medical evidence. Follow these steps to help to build a strong case:

- Work closely with your doctors: Provide them with copies of each policy's TPD definition so they can tailor their reports accordingly.

- Seek comprehensive assessments: Depending on your condition, this might include reports from specialists, psychiatrists, occupational therapists, or rehabilitation providers.

- Ensure reports address specific criteria: Medical evidence should clearly state how your condition meets each policy's definition of ‘total and permanent disability’.

- Be prepared for insurer examinations: Insurers often request independent medical examinations. Be consistent here and try to give the same information you gave to the doctor(s) who first assessed you.

- Document functional impacts: Ensure medical reports detail how your condition affects your ability to work and perform everyday activities. This is essential. Be frank about what effect your condition has had.

Remember that inconsistencies in medical evidence across different claims can create complications and ultimately slow down the process. ‘Be consistent’ is the main advice here.

Professional Support for Complex Claims

Given the complexity of managing multiple TPD claims, you may wish to seek out professional legal advice and support. TPD claims specialists have submitted hundreds of claims and know exactly what needs to be done to maximise your chances of success. Here’s an overview of how they can assist in your claims:

A TPD claims specialist can:

- Review all your policies to identify potential entitlements

- Advise on the optimal order for submitting claims

- Coordinate medical evidence to satisfy different policy requirements

- Manage communication with multiple insurers

- Handle disputes or appeals if claims are rejected

When selecting a specialist, look for:

- Experience specifically with superannuation TPD claims

- A track record of handling multiple claims simultaneously

- Clear fee structures (many work on a no-win, no-fee basis)

- An understanding of the latest legal developments in TPD claims

The right professional support can significantly increase your chances of successful outcomes across all your claims, so it’s well worth looking into.

Financial Considerations

Let’s imagine for a moment that the multiple claims have been successful. What are some other considerations to factor in here? Well, firstly, your financial situation may be impacted. Here are some key things to consider:

- Tax implications: TPD benefits paid into super are generally not taxed until withdrawn. Tax may apply when withdrawing as a lump sum, depending on your age and circumstances.

- Interaction with other benefits: TPD payouts typically don't affect Workers' Compensation or Income Protection payments. However, they may impact Centrelink entitlements if withdrawn from super.

- Long-term planning: Multiple lump sums require careful financial planning. Consider consulting a financial adviser to help manage these funds for immediate needs and long-term security.

- Effective use of funds: Prioritise allocating money for medical care, rehabilitation, debt repayment, and ongoing expenses.

At the end of the day, TPD benefits are designed to provide financial support when you can no longer work, so careful management of these funds is essential for long-term security.

Taking Action: Your Next Steps

So, let’s recap. If you're facing a total and permanent disability and believe you may have multiple TPD policies, here are your immediate next steps:

- Gather information: Collect details of all your superannuation accounts, past and present.

- Confirm coverage: Contact each fund to verify if TPD insurance was active when you became disabled.

- Request documentation: Obtain complete policy documents from each fund.

- Seek professional advice: Consider consulting a TPD claims specialist for an initial assessment of your situation.

- Begin medical documentation: Work with your doctors to build the appropriate medical evidence.

As with many lengthy processes such as this: the sooner, the better. Gather everything you need and submit things quickly to maximise your entitlements across all your policies.

Final Thoughts

Having multiple TPD policies across different super funds is a great way to gain access to much-needed financial support at a time when you need it most. Understanding your entitlements and navigating the claims process effectively requires knowledge, organisation, and strategic planning.

By identifying all your policies, getting to grips with their different definitions and requirements, building strong medical evidence, and considering professional support, you can boost your chances of successful outcomes on multiple claims.

Remember that each policy represents a separate contract you've paid for through your super contributions. You're entitled to claim on each one if you meet the criteria, which could potentially make vital funds available.

To enquire online about TPD claims, call 1800 960 482. No Win, No Fee, No Catch®. Our guarantee: In the unlikely event your case goes to court and you're unsuccessful, we'll cover the costs. This way you won't pay a cent to us or anyone else. In nearly 30 years, we've never had a single client out of pocket.